The Greeks Say Otherwise.

Most first-time options traders start the same way: stare at the payoff chart until it looks profitable, then hit submit. The chart says you'll make money if the price drops. Good enough, right?

But the payoff chart only tells you what happens at expiry. It doesn't tell you what happens between now and then. That's where the Greeks come in.

Let's walk through an example. (This isn't a trade recommendation. It's a case study. The fastest way to understand Greeks is to watch them break a strategy in real time.)

The Setup

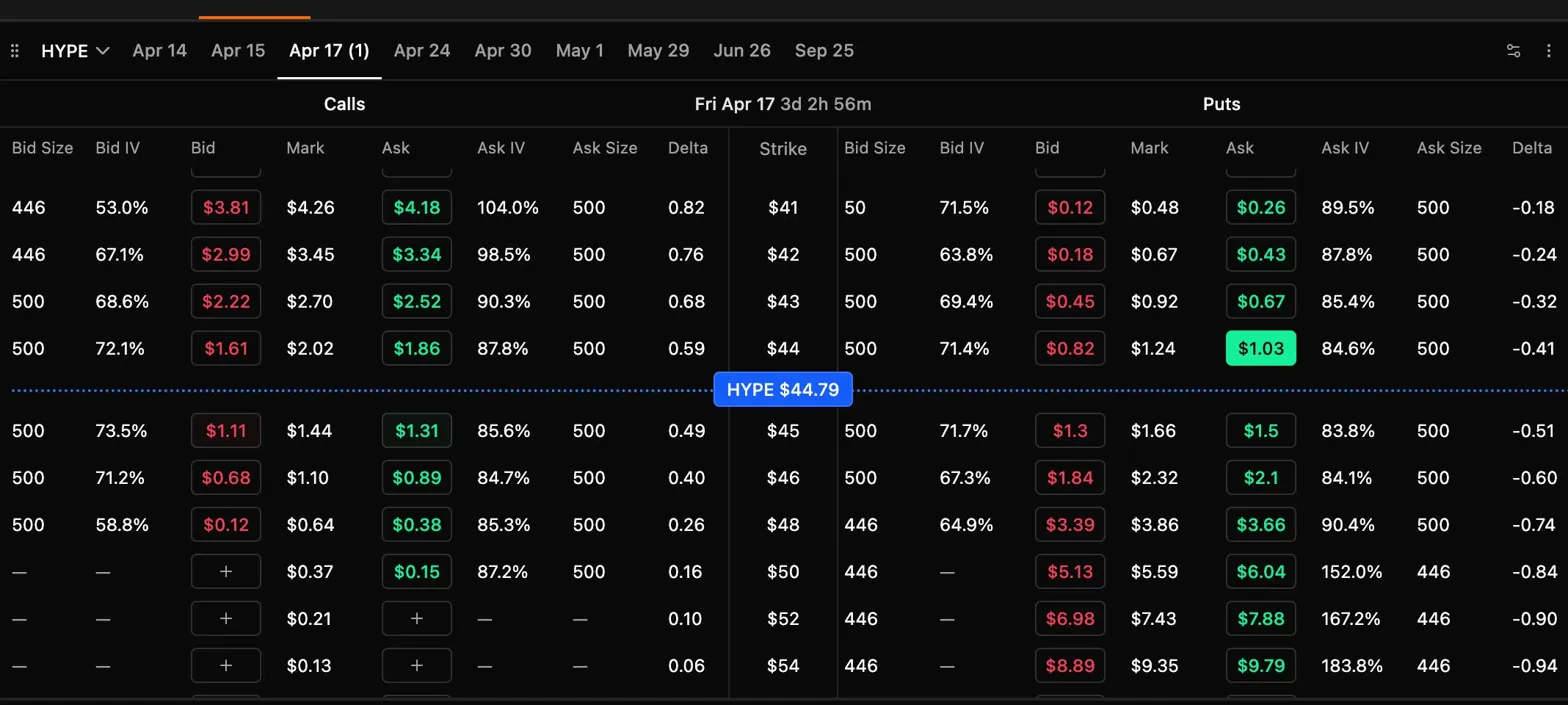

April 14. HYPE just pumped to ~$44.79 and implied volatility (IV) is elevated across expiries. You decide to work with the Apr 24 expiry to give the trade more time to play out.

Your thesis: sell volatility, with a bearish lean on price.

If you only wanted to sell vol with no price opinion, you could use delta-neutral strategies like short straddles or iron condors. But you also expect a retracement. So you need a structure that's bearish AND short vol.

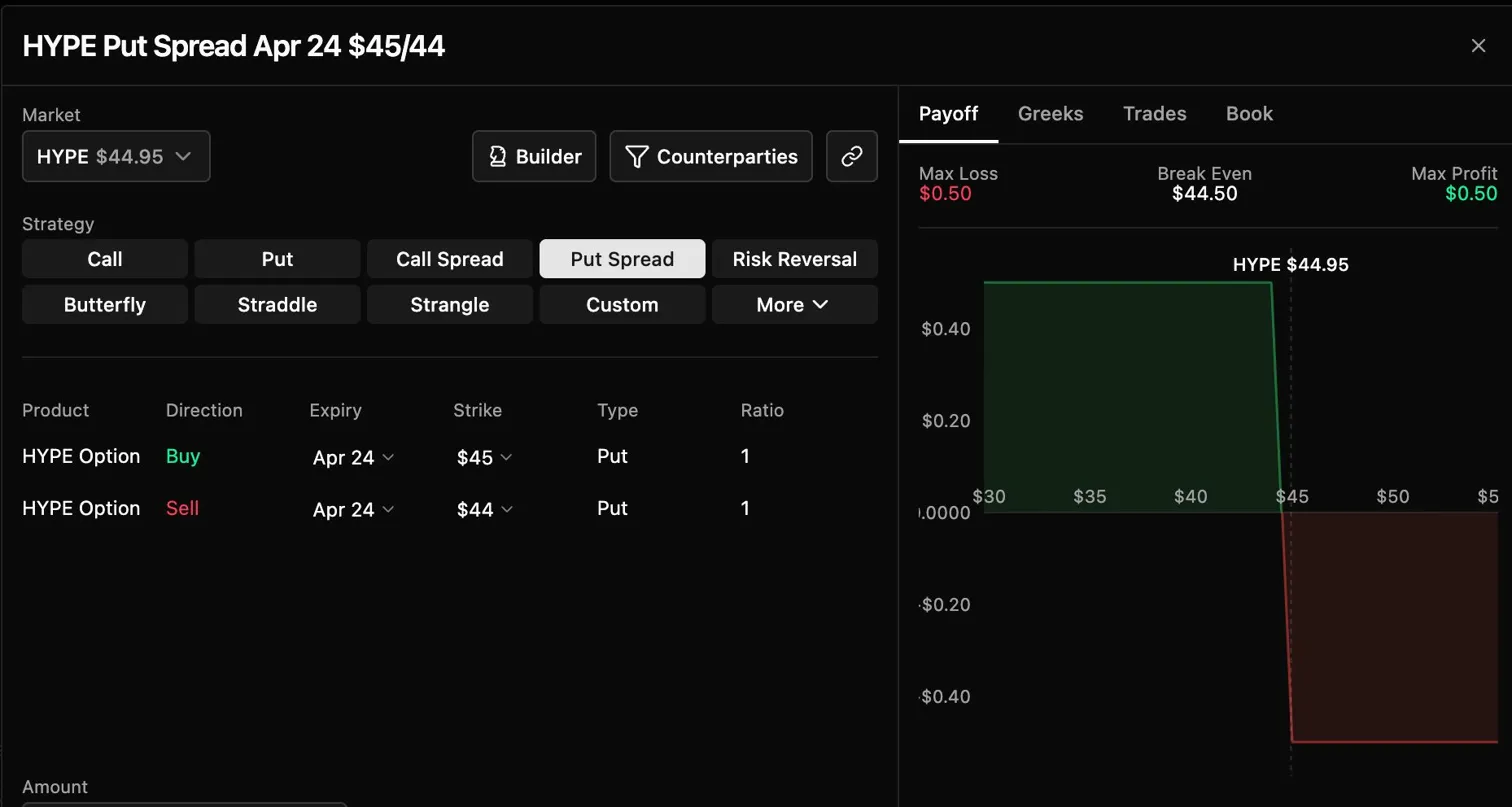

The Trap: Bear Put Spread

So you open the Strategy Builder, set it to Bearish, and build a put spread. Buy the $45 put, sell the $44 put. The payoff chart confirms it: profit if HYPE drops below $44.48.

At this point, most beginners would hit submit. The payoff chart looks right, the direction is right. Why look further?

But there's a tab next to Payoff that most first-timers skip: Greeks. Click it.

Vega: +0.00036. Theta: -0.00122.

The numbers look small, but the signs are what matter:

- Positive vega: You wanted to sell volatility, but vega says you're buying it.

- Negative theta: You wanted time to work in your favor, but theta says every day that passes costs you money.

The payoff chart didn't lie. But it didn't tell the whole story either. This bear put spread is a debit trade. You paid premium upfront, and that premium is loaded with implied volatility. You need IV to stay elevated or price to move enough to justify what you paid. That's the opposite of selling vol.

What the Greeks Actually Tell You

Before fixing the strategy, here's what those numbers mean.

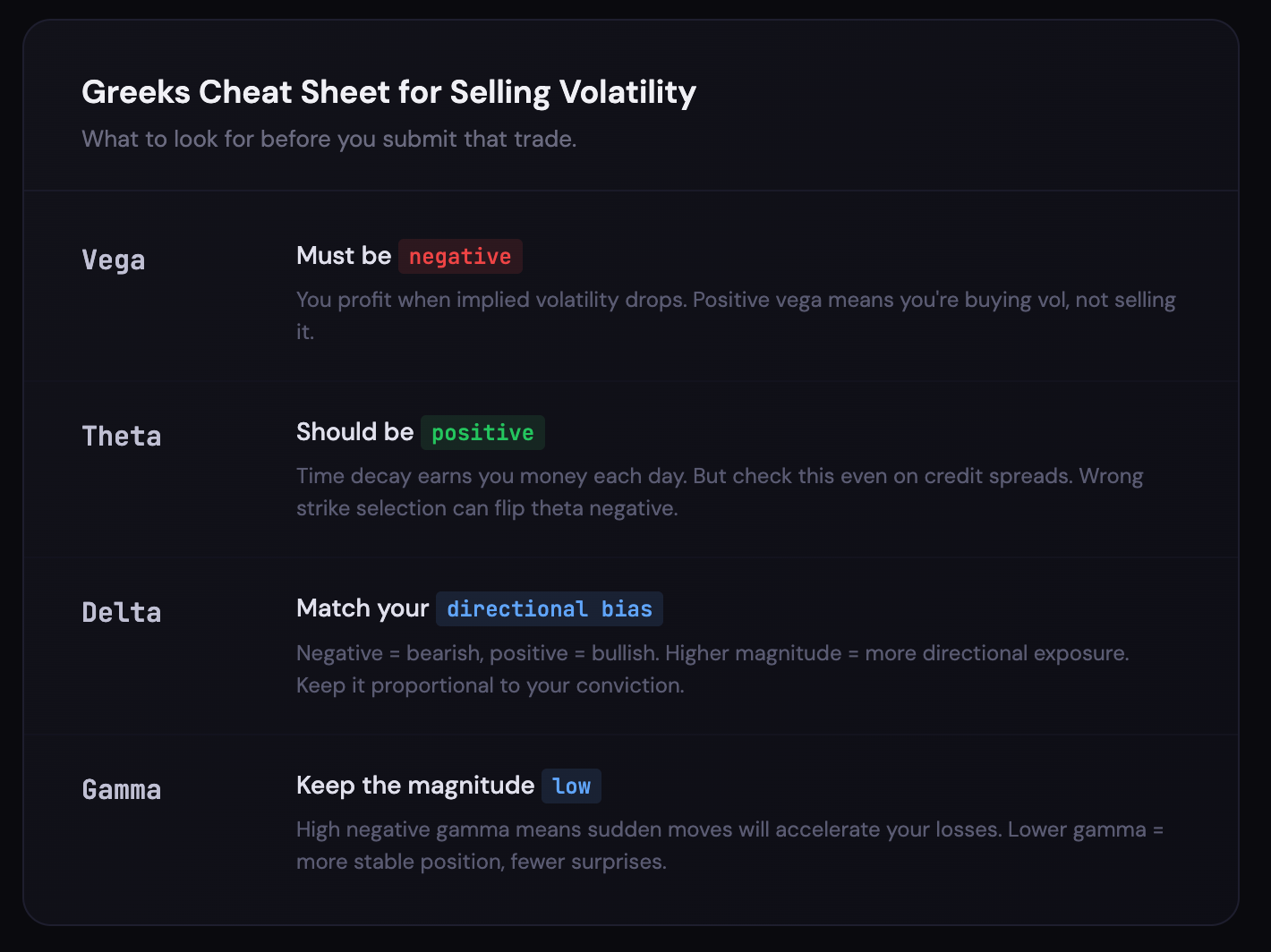

- Delta: How much your position gains or loses per $1 move in the underlying. If your delta is -12 and HYPE goes up $1, you lose ~$12.

- Vega: Your exposure to implied volatility. If your vega is -0.17 and IV drops by 1%, you gain ~$0.17.

- Theta: How much value your position gains or loses per day from time passing. If your theta is +0.44, you earn ~$0.44 every day just by holding the position.

- Gamma: How fast your delta changes. If your gamma is -5.48, a $1 move in HYPE shifts your delta by 5.48, accelerating your losses on sudden moves. Lower gamma means a more stable ride.

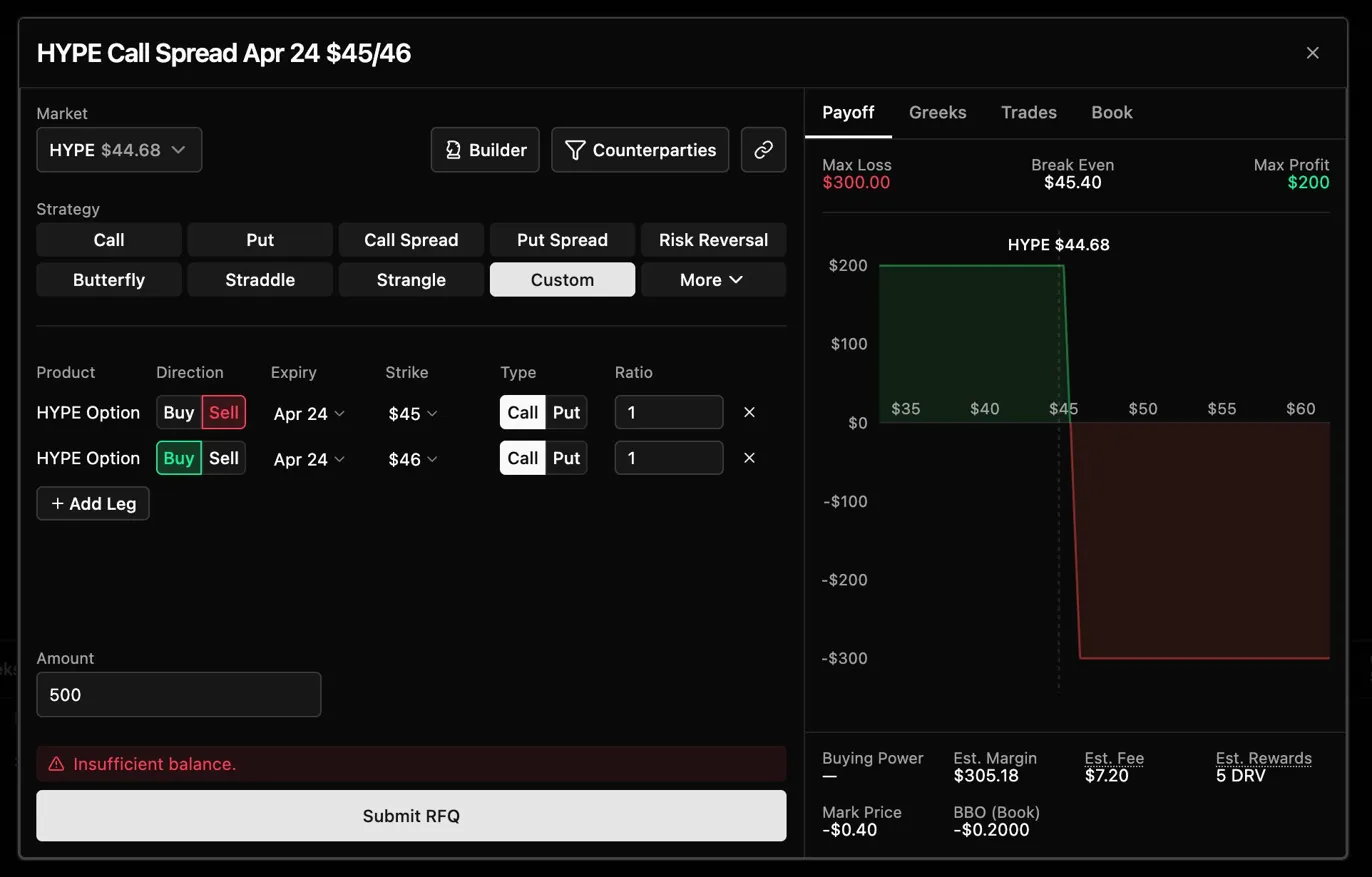

The Fix: Bear Call Spread

The bear put spread failed because you paid to enter the trade. When you pay premium, you're buying the implied volatility baked into that price. That's long vol by definition.

So what if you collected premium instead? That's a bear call spread. Sell a call, buy a higher strike call. You get paid upfront.

First Attempt: $45/$46

Sell the $45 call, buy the $46 call. You collected premium. The payoff chart shows profit if HYPE stays below $45.

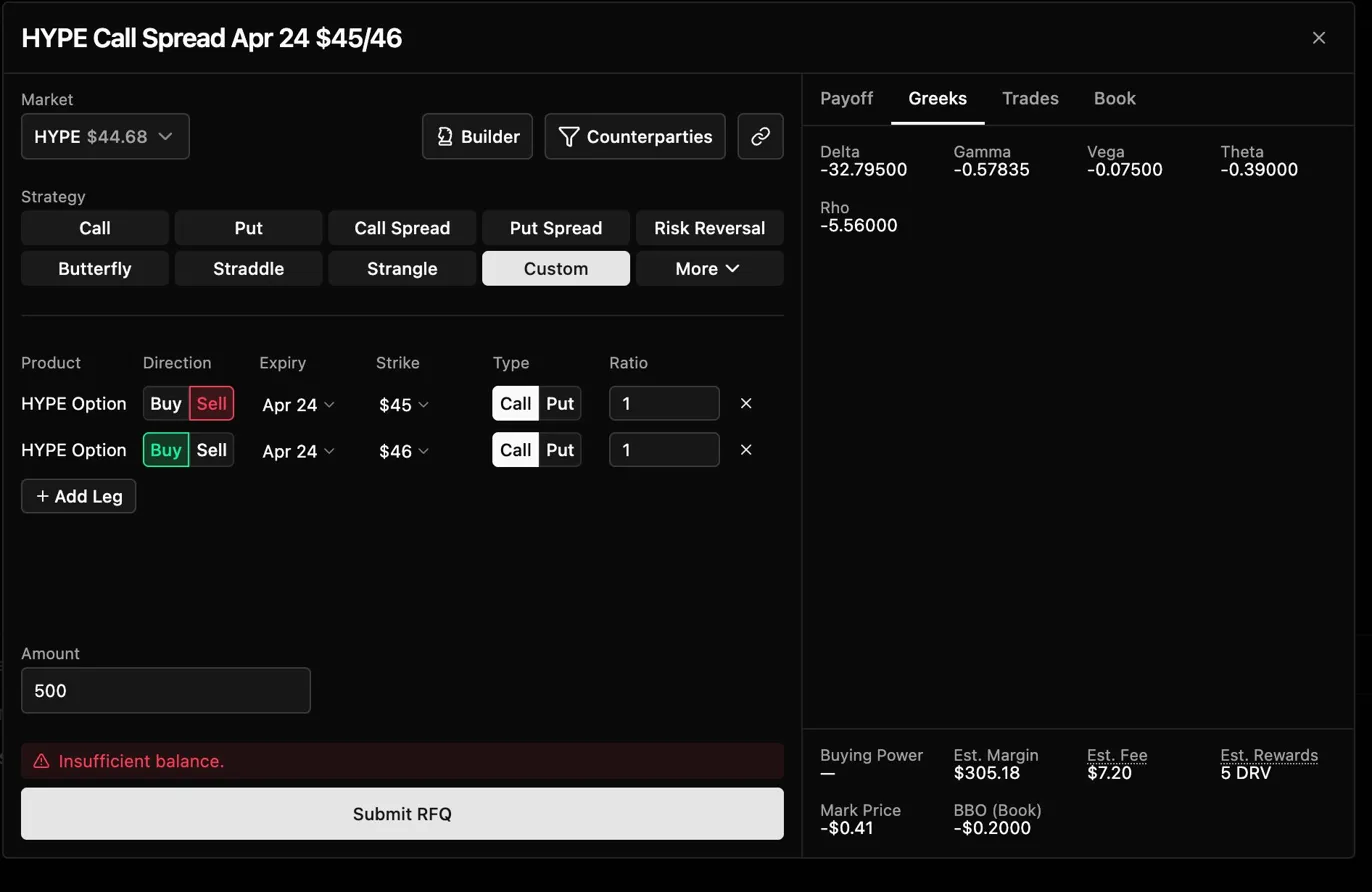

Now, check the Greeks:

- Vega is now negative (-0.075). That's progress. Collecting premium instead of paying it flipped the vol exposure. You're now short vol.

- Theta is still negative (-0.39). Even though you collected premium, time decay is working against you. That might seem odd for a credit spread. But this is real data from Derive's Strategy Builder at the time. And this is exactly why you need to understand your Greeks.

Half fixed, half broken.

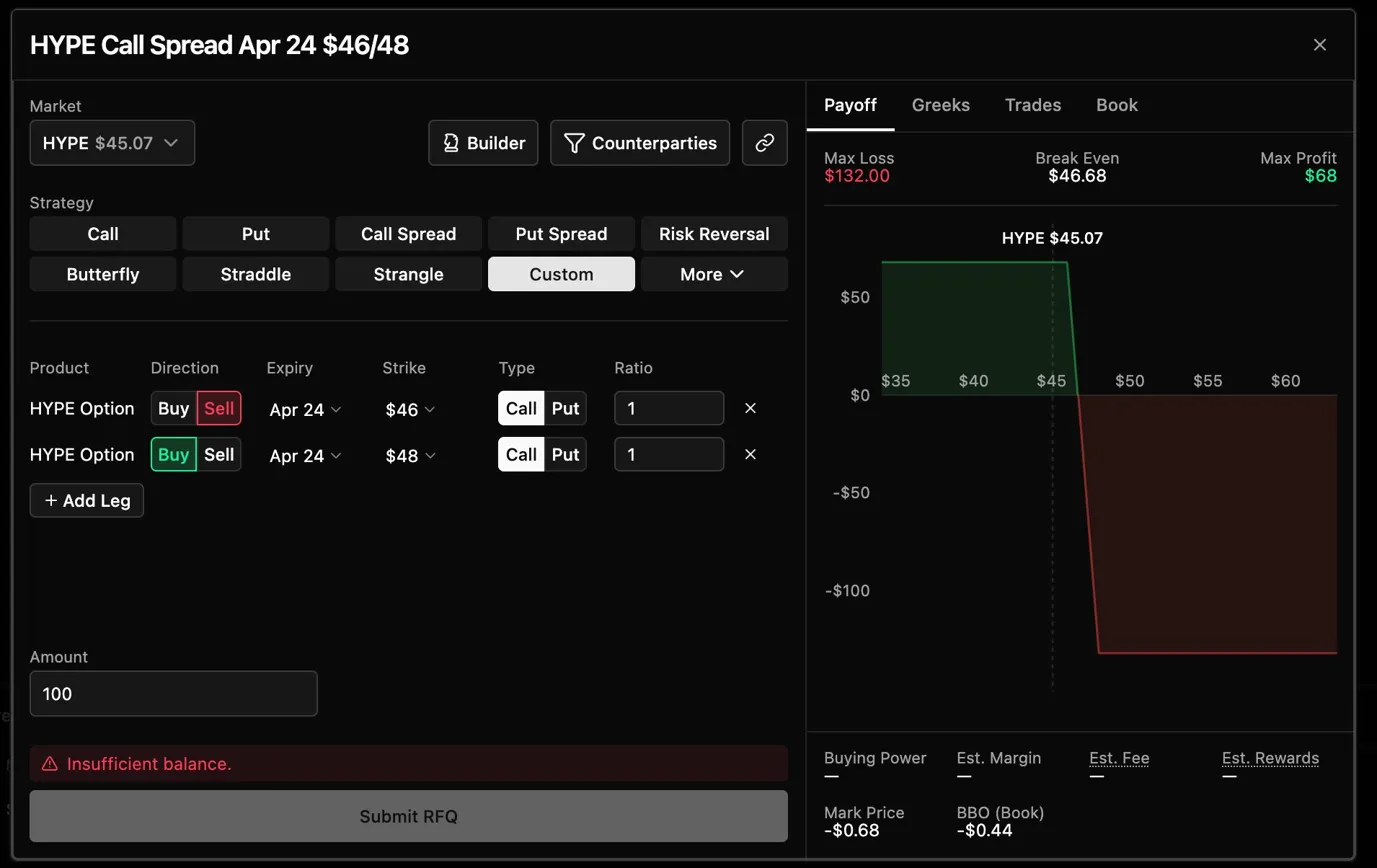

Second Attempt: $46/$48

Widen the spread. Move the short leg further from spot. Sell the $46 call, buy the $48 call.

Every single Greek is now aligned with the thesis.

The Greeks as Your Strategy's Lie Detector

The payoff diagrams of the bear put spread and bear call spread look nearly identical at expiry. Both profit if HYPE drops. But the experience of holding them is completely different.

The bear put spread needs HYPE to actually move down to make money. The bear call spread profits from HYPE just staying put, drifting lower, or from IV simply dropping. Theta and vega do the heavy lifting.

The difference comes down to credit vs debit:

Credit spread (you got paid) = short vol, positive theta. Debit spread (you paid) = long vol, negative theta.

But as the $45/$46 example showed, even this rule has exceptions. The only way to know for sure is to check the Greeks tab before you submit your strategy

Greeks are a snapshot in time. They change as price moves and time passes. Always recheck if conditions shift significantly.

This content is for educational purposes only. Not financial advice.